Briefing Note for councillors: RFO update on the Councils finances

Issued to: Town Council 22nd June 2020

Purpose of Report

To provide Councillors with updated information regarding the general reserve, accounting changes and current ear marked reserves (EMRs)

General Reserve

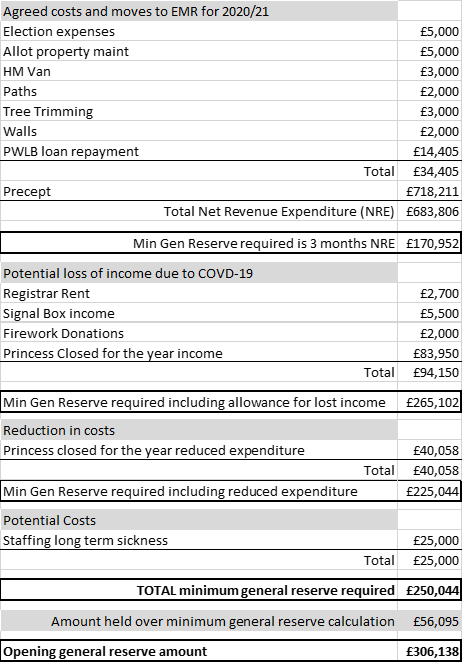

As of the 31st March 2019 the Town Council’s general reserve was £327,951. During this year the Council had agreed specific items of expenditure would be spent from the general reserve so it was expected that the general reserve would have reduced and as of the 1st April 2020 the amount was £306,138.

In order to assess that the Council has an appropriate level of general reserve please see the spreadsheet with the net revenue expenditure calculations. Proper practices suggest that a Council of this size should hold a minimum of three months’ net revenue expenditure (NRE). To calculate the NRE, use the total of all previously agreed costs for the year where money is allocated to future projects, remove this total from the precept amount and divide the residue by 4 to arrive at the minimum amount to be held.

However, this is an unusual year and the Council will be aware that some of the anticipated income and expenditure that was budgeted for will not happen or be reduced. It is therefore necessary to include some further adjustments to try and provide a more accurate projection of the Council’s financial position. Being based on projections they may change.

Several sources of income will be affected by Covid-19. Therefore they have been removed the total sum of the projected income from this figure.

The projected reduction in the costs at the Princess has been added.

The risk of long of term sickness is currently increased and therefore a sickness contingency amount has been included which would pay for a locum Clerk or RFO should they be required.

The projected minimum general reserve required based on these calculations is £250,044. The Town Council held £306,138 as of the 1st April 2020.

The following spreadsheet shows how this figure has been arrived at.

Note that the Town Council has received two grants in support of reduced income and fixed costs from Arts Council Fund and SDC COVID-19 Business Grant, they will support £31,927 of costs. These are not taken account of in the above figures as they are not part of the general reserve.

Accounting Changes

When the Joint Burial Committee was dissolved on 31st March 2019 all the income and expenditure came into the Council’s accounts in a similar format as it was previously. However, having worked closely with the Deputy Clerk it has been agreed that some changes should be made to provide a clearer picture of the Council’s total ear marked reserves and streamlining the Burial Committee’s finances. The ear marked reserves have been moved from the burial committee section of the accounts and are now included in the same list as the rest of the Town Council’s reserves. The cemeteries were all accounted for separately but for simplicity we have merged the three cemeteries in to one code, providing the required information.

Ear Marked Reserves (EMRs)

As of 31st March 2019 the total amount held in EMRs was £611,831.65 and as of the 1st April 2020 there was £687,381.41. It is important to note that included in this updated amount is £52,775 of new restricted funds. £46,375 Community Impact Mitigation funds, £5,400 Hinkley Tourism Action Partnership funds and £1,000 from the Police Community Trust. These funds can only be spent in the areas covered by the grants themselves.

Policy implications

Financial Regulations

3.6 The General Reserve is a contingency to cushion the impact of unexpected events or emergencies and to avoid unnecessary temporary borrowing.

3.7 The Council considers a prudent level of General Reserves to be three to six months’ net revenue expenditure.

Overview

The amount of general reserve currently held is within the guidelines within the proper practices.

The ear marked reserves were reviewed extensively at budget planning and now stand at a total of £687,381.41.

The movements of the Burial Committee’s accounts should make it easier for the Council to see all the unrestricted ear marked funds when making financial decisions and the merging of the cemeteries’ accounts provides a more streamlined view of this committee’s financial commitments.

Report author: Sally Jones

Report Date: 10th June 2020